Rich Karlgaard, the publisher of Forbes magazine, mentioned my book in his article:

Rich Karlgaard, the publisher of Forbes magazine, mentioned my book in his article:

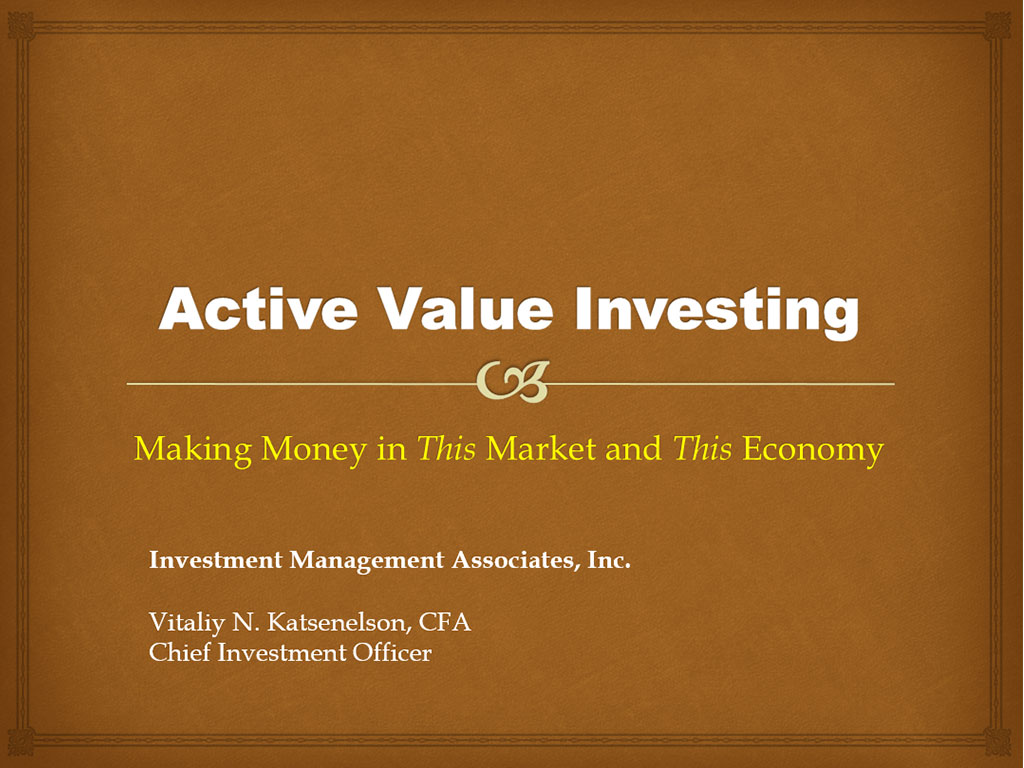

The new Benjamin Graham is Vitaliy N. Katsenelson. I highly recommend Katsenelson’s book, Active Value Investing: Making Money in Range-Bound Markets (Wiley, 2007). I like to think the old Ben Graham would have recommended it, too.

0 comments